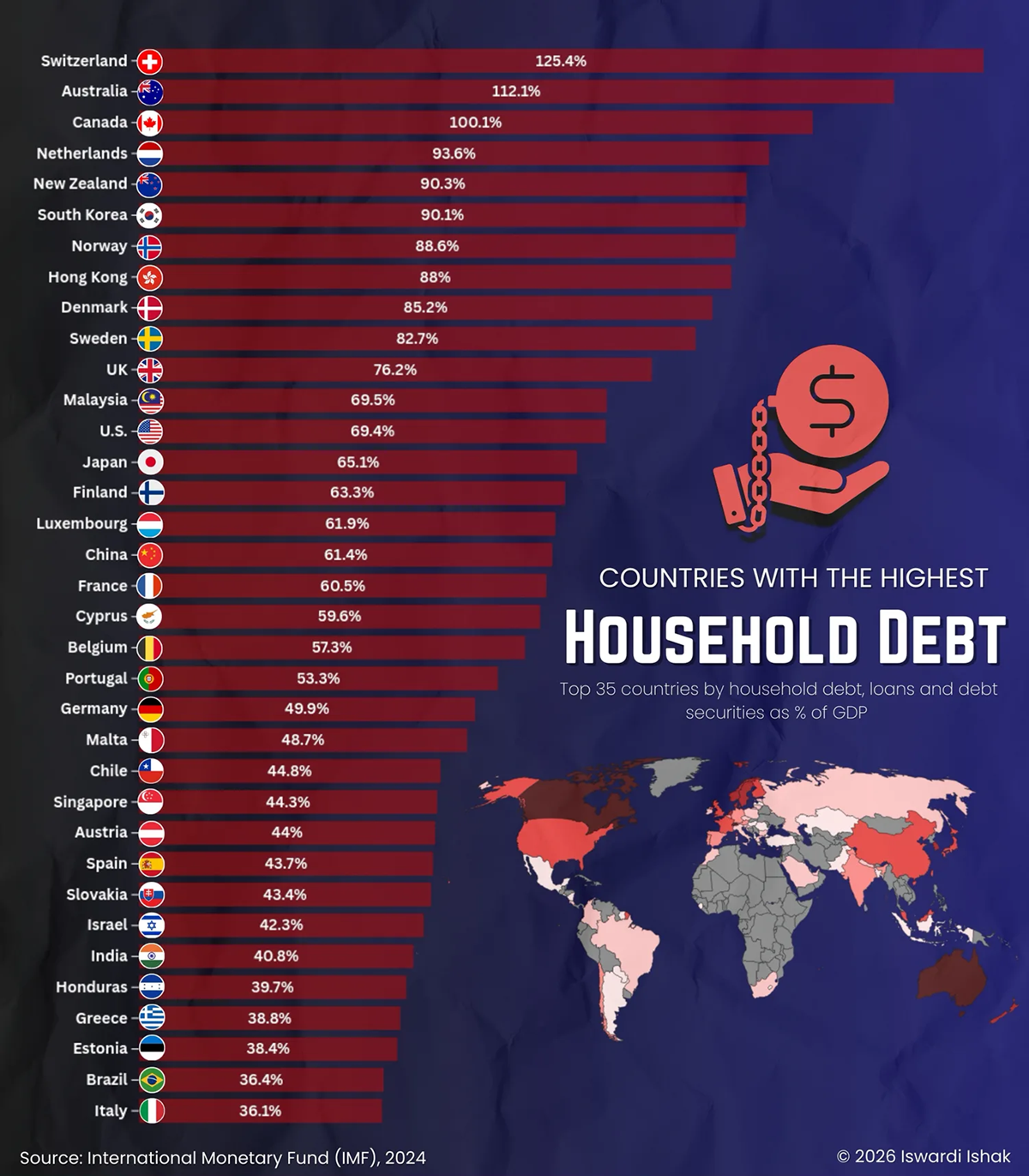

(9 February 2026 – Global) The International Monetary Fund (IMF) has released new data revealing the countries with the highest levels of household debt with important implications for economic growth and vulnerability to rising interest rates and “black swan” events.

Switzerland tops the list with household debt including includes mortgages, car loans, credit card debt and personal loans exceeding 125 percent of GDP, followed by Australia (112 percent) and Canada (100 percent) as two countries renowned for overpriced residential housing markets.

“In the event of economic shocks, high household debt levels result in non‑performing loans that weaken bank balance sheets and spread to other financial institutions through the contagion effect. This could result in an unstable financial sector that restricts lending to profitable investments and deserving households. Ultimately, household consumption and investment decrease, thereby lowering economic growth” the IMF study notes.

“The metric is often used as a barometer for financial risk and vulnerability at the household level. While credit access enables household consumption and property ownership, it also creates exposure to economic shocks. High household debt can constrain economic growth when families divert income to servicing debt rather than spending or saving. It also increases sensitivity to interest rate hikes, which raise repayment costs.”

“Research from the Leibniz Institute for Financial Research highlights how household debt, when misaligned with wage growth or asset prices, can trigger financial instability. Elevated household debt goes beyond being a macroeconomic statistic, and has the potential to amplify downturns and reduce resilience at both the household and national level.”

Source: Visual Capitalist, Voronoi Data Researcher, Iswardi Ishak