(6 November 2025 – Australia) National Australia Bank risks losing its status as the country’s top business lender as disappointing earnings and more competition prompt questions from investors and analysts about chief executive Andrew Irvine’s strategy.

The major bank said underlying profit in the 12 months to the end of September grew 1 per cent and net profit fell 2.9 per cent, below market expectations, as margins slipped in the face of a push from Commonwealth Bank and Westpac to grow market share in business lending.

“Competition is fierce, and it’s fierce because it’s the best part of the banking market to be playing in … returns are better in business banking, so everyone wants to be NAB,” said Irvine as he presented the results.

“We have shown in the last year, particularly in the last six months, that we can both defend and extend our position and not give away margin.”

A desire for CBA, Westpac and even Macquarie to grow their business lending has been a constant over the year, lured by the promise of higher profits and a long period of competition for mortgages, where the two major banks have traditionally been stronger performers than NAB.

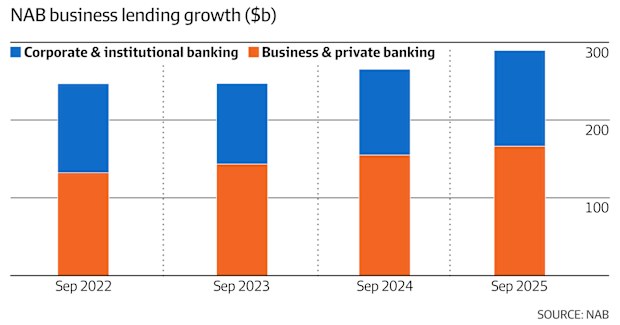

NAB’s net interest margin – a key measure of profitability in banking – in business and private lending was 3.02 per cent in the six months to September 30, up from 3.01 per cent in the first half. But it remains well below the 3.11 per cent margins the bank saw in the previous year.

Matthew Wilson, an analyst at Jarden, questioned Irvine’s confidence when it came to business lending, adding that NAB could no longer claim to be the unequivocal leader with CBA better placed for growth.

“Why doesn’t NAB publish MFI statistics [for the business bank]? They don’t suit their narrative because CBA is number one in MFI,” Wilson said referring to “main financial institution” figures that show how many businesses would consider NAB to be their primary bank.

“It’s not unequivocal for NAB to claim the leadership in business banking.”

Wilson said NAB’s business bank had lower returns than CBA, which made it more difficult for it to grow its market share. Comparing NAB and Westpac, Wilson said the latter won on asset quality and capital.

Argo Investments’ senior investment officer Andy Forster, whose fund holds shares in the bank, said: “Today, NAB still seems to be holding out, and if anything grown, but the big unknown is whether they can continue to.”

Westpac in May hired a new head of business banking, Paul Fowler, who arrived from CBA.

He is one of new Westpac chief executive Anthony Miller’s key hires as the former Deutsche Bank executive attempts to reshape the lender by cutting costs and expanding into business lending.

Miller also hired chief financial officer Nathan Goonan from NAB.

Westpac, which reported its result earlier this week, said business loans rose 15 per cent to $115 billion, and loans from the institutional bank were up 17 per cent to $118 billion – far surpassing the mortgage growth rates.

But Irvine said there was “good momentum”, with the increase in underlying profit largely driven by a strong performance in the second half of the year. Cash earnings of $7.1 billion were little changed, but NAB’s cost growth of 4.6 per cent outpaced a 1.2 per cent increase in revenue.

Irving pointed to margin improvement in the past six months, in response to criticism from CBA’s banking boss Mike Vacy-Lyle that NAB and Westpac were adopting riskier pricing to defend or grow their business market share.

“We are making good progress on … growing business banking, driving deposit growth and strengthening proprietary home lending,” he said.

“This has been supported by targeted investments in front-line bankers and technology-enabled solutions delivering simpler, faster and safer outcomes.”

Irvine, who came under scrutiny earlier this year over his behaviour at a client event, took home $7.6 million in total remuneration in the last financial year, according to NAB’s annual report.

That included $2.5 million in fixed pay and a variable reward of $1.04 million in cash. The rest comprised mostly share-based short and long-term incentives.

The bonus payout was 69 per cent of Irvine’s fixed remuneration, compared with a payout range of 62 to 92 per cent across all group executives.

The annual report noted that a senior manager had received coaching or a warning, or faced “other remedial action” in the last year.

“The group CEO, group executives, and other senior leaders are expected to actively demonstrate strong risk management to set the ‘tone from the top’ on expectations and behaviours,” the report to investors read.

In July, The Australian Financial Review reported that major investors had raised serious concerns about Irvine’s management style and drinking at customer meetings and events with directors, prompting the board to increase mentoring and provide more leadership development.

NAB shares fell 3.3 per cent, or $1.47, to close at $43.06. The S&P/ASX 200 rose marginally, adding 0.3 per cent, while shares at CBA, the country’s largest bank, rose more than 1.2 per cent, or $2.22, to $178.57.

Although its business bank comes under pressure, NAB gained traction in its retail division, with cash earnings there up 9.9 per cent – the strongest growth of its four business streams – as deposits and mortgages rose.

Owner-occupied home loans grew by 4.1 per cent to $237 billion over the year, and investor loans by an even stronger 5.7 per cent to $126 billion.

Irvine’s push to write more mortgages through the bank’s own channels, rather than through brokers, is likely to improve its margins. NAB wrote 41.4 per cent of loans through its own channels, up from 35.4 per cent.

Investors will get a final, fully franked 85¢ dividend, the same as last year.

Source: Australian Financial Review