(17 October 2025 – Australia) Australia’s corporate banking landscape has split into two distinct camps.

On one side are the transaction-led banks, dominating cash and payments flows. On the other are the trade-led institutions, leveraging global supply chain expertise to win client primacy.

East & Partners’ latest Trade & Supply Chain research highlights this divide, even amongst businesses with active trade facilities in place — and what it means for future growth.

The Transaction-Led Anchors: NAB and CBA

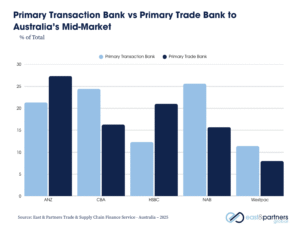

NAB and CBA continue to lead in commercial transaction banking with 25.6% and 24.4% of the mid-market transaction banking relationship share respectively, reflecting their strength in domestic payments, liquidity, and working capital solutions.

However, their trade finance penetration into this base remains modest, despite all of them having international trade needs, capturing around 15–16% of primary trade and supply chain relationships. While these banks excel in cash management and integration, the data suggests they face challenges converting this dominance into broader cross-border financing and supply chain engagement.

For NAB and CBA, the opportunity lies in bridging the domestic-to-global gap — embedding trade solutions into their strong transaction franchises to prevent client leakage to international competitors.

The Trade-Led Challengers: ANZ and HSBC

By contrast, ANZ and HSBC have built their strength around trade, supply chain, and cross-border flows, capturing 27.3% and 21% of the segments’ primary trade relationships respectively. Both banks have leveraged their global networks and deep treasury expertise to anchor relationships through trade first, and then expand into payments, FX, and working capital.

Yet, their transaction banking shares — around 21% and 12% respectively — show they still face barriers converting these global relationships into full-service, multi-product primacy.

The Strategic Middle Ground

Westpac, Citi, and emerging challengers sit between these two models — balancing domestic cash management strength with selective trade wins. However, their combined share remains relatively small, suggesting the market’s middle ground is still up for grabs.

What It Means for 2025

This trade-versus-transaction divide reveals a bigger strategic question:

Will banks continue to compete in silos, or will they integrate trade and cash solutions into a single, frictionless client experience?

The data suggests that’s where the market is heading. As corporates demand simplicity, visibility, and end-to-end connectivity, the most successful banks will be those that unify their trade and transaction propositions under one relationship strategy.

For senior bank leaders, the takeaway is clear:

-

Transaction-led banks must globalise their offering.

-

Trade-led banks must embed themselves in domestic flows.

-

Both must invest in client-level intelligence to understand how treasurers choose and manage multi-banking relationships.

In short, the next competitive frontier won’t be defined by who leads in trade or cash management — but by who owns the whole cash-to-supply-chain journey.