(15 December 2025 – Global) The new year heralds growth and opportunity in 2026 for banks across APAC, EMEA and the Americas but not without challenges as highlighted by CFOs, treasurers and key decision markets as part of East & Partners proprietary research.

In the year of the Fire Horse (Bing Wu) according to the Chinese Zodiac, leading corporates are firmly “on the move” as they seek enhanced treasury management capability, relationship management and specialist advice amid the cavalcade of innovative AI solutions set to face closer scrutiny as product, service and customer utilisation accelerates.

Global

More than ever, cash management and transaction banking represents the core foundation for customer engagement. Automation, real-time analytics and cash flow forecasting have triggered an “arms race” for leadership among CFOs and treasurers more likely than ever to switch their transaction banking relationship in part or full. Heavy weights including JPMorgan, Citi, Standard Chartered and HSBC have successfully fended off stern competition from regional majors in key markets, however a fight back from fast growing challengers such as BNP Paribas and BOC is observed in East & Partners klong running Cash & Payments reporting.

Customer loyalty is deteriorating rapidly as customer switching intent increases to a record high in multiple markets. Incumbent leaders face growing pressure limiting wallet share “leakage” as CFOs “panel bank” more aggressively than ever.

Global trade will continue to be defined by the shift away from globalisation and free trade towards aggressive “on shoring” and protectionism, led by the United States. While corporates have been quick to respond and manage uncertainty that was a feature of the first half of 2025, markets remain on a knife edge for the continued unpredictable evolution in trade policy.

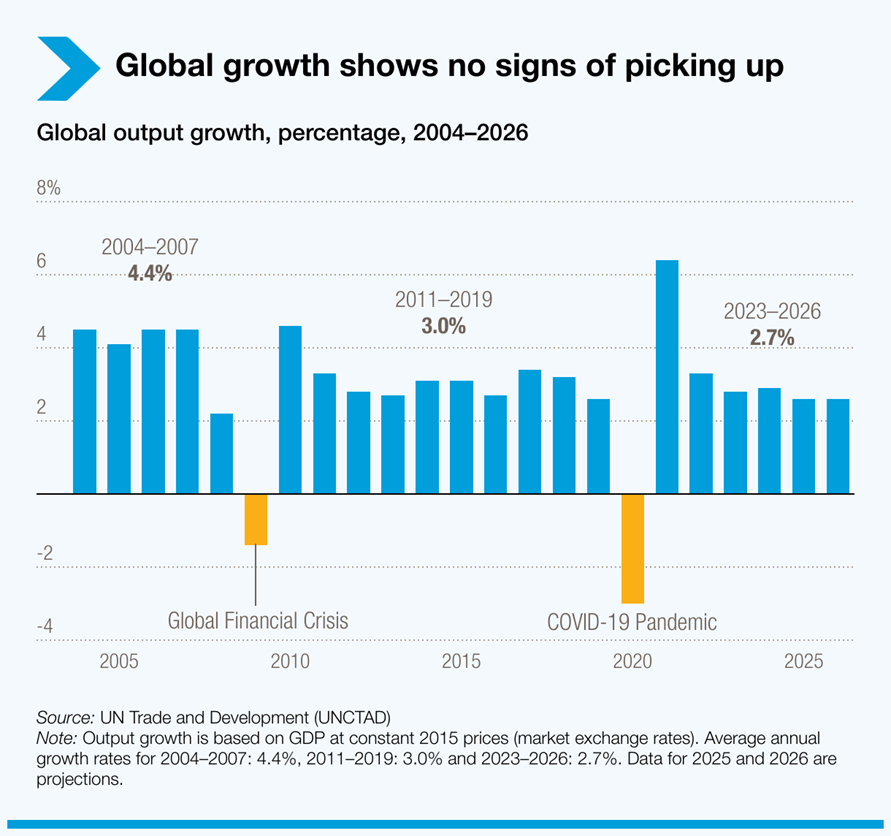

With global growth GDP forecast by MEI to moderate at 3.1 percent in 2026 from 3.2 percent in 2025, and as low as 2.6% according to UNCTAD, the Top Five risks for the global economic outlook according to Apollo include:

- US economy “running too hot” as a result of a fading trade war shock and inflation moving up from an already elevated level

- The global industrial renaissance boosts global growth with more and more countries focusing on homeshoring advanced manufacturing capacity, investing in infrastructure, energy, defence and supply chains

- The new Fed Chair lowers interest rates purely as a result of political interference

- AI bubble bursting resulting in sluggish capex growth

- Pressure on credit spreads and rates stemming from higher supply of fixed income as government deficits blow out

Source: UNCTAD

APAC

As the global trade finance gaps remains steady at US$2.5 trillion according to the Asia Development Bank (ADB), concern is mounting that readily available solutions will not be pursued fast enough to close it and enable access to credit for SMEs. SMEs are disproportionately affected the most by the trade finance gap, with two thirds of trade finance applications by SMEs rejected, in contrast to a mere seven percent for large corporates.

After the Swift ISO20022 standard “went live” across major global payment networks, enhanced cash visibility is no longer the exception to the norm. Synchronisation of real time payments networks across the Asia Pacific region will continue to see greater integration with an onus on onboarding ease and support.

Businesses in Australia are tasked with doing more with less as mounting productivity challenges continue to weigh on the economy, especially SMEs as the “engine room” of growth and employment. The Productivity Commission reports that while SMEs account for more than half of Australia’s GDP, they lag large firms in productivity performance by around 50 percent, broadly consistent with other OECD member nations. Round 23 of the biannual ScotPac SME Growth Index highlights that more than one in five SMEs (21 percent) say productivity barriers are driving up wage costs and holding back innovation and growth.

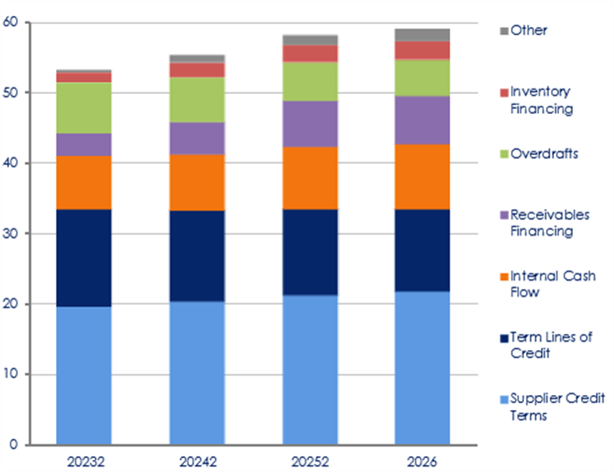

Is Private Credit the answer for corporates seeking relief for working capital constraints as regulators take a more active stance?

Forecast Non-Trade Finance Funding Solutions Used

% of Total Trade Financing Needs

Source: East & Partners Asia Trade & Supply Chain Finance Service (N: 926)

EMEA

As the European Union reviews its sustainability regulatory framework and seeks to revise its priorities following a shift from voluntary to mandatory corporate ESG obligations, the global mood continues to shift quickly on net-zero policies.

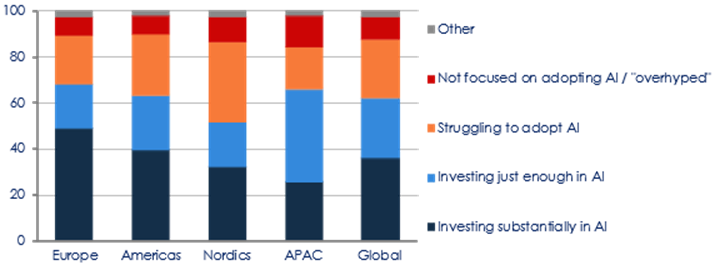

Banks across the UK and Europe are open to partnering with nimble Fintechs to deliver new technology faster and overcome legacy systems limitations, a key area of focus for the Tech Mahindra Bank of Tomorrow report. Agentic and generative AI (GenAI) have moved beyond the experimental phase to become transformative tools reshaping CX, risk management, compliance and product innovation. The research shows over 1 in 3 financial institutions (FIs) are already investing aggressively in GenAI to capture the early-mover advantage. (37%). European banks (49%) are outpacing peers in AI investment by a considerable margin, ahead of Americas (39%), the Nordics (32%) and APAC (26%). However, 1 in 4 banks still struggle to adopt new AI solutions, risking being left behind (25%).

In Africa, Banks are also open to partnering with telecommunications providers also to reach scale or “leapfrog” development issues encountered by banks grappling with major overheads in developed markets.

Risk management has fast become a competitive differentiator for leading Banks as corporates struggle to keep ahead of emerging cyber threats and mounting compliance concerns across the treasury function. FX risk management is an excellent example, with a concerted shift away from FX Options towards Forward FX gathering pace as treasurers take a more active stance to limiting their currency exposure. Where are CFOs and treasurers sourcing advice and solutions to remain ahead of the curve and how can Banks incorporate greater support into their relationship management model?

AI Investment Outlook

% of Total

Source: Tech Mahindra Building the AI-Driven Bank of Tomorrow (N: 150)

Americas

The United States represents the forefront of investment and development for Stablecoin uptake following the passing of the GENIUS Act. With an almost daily announcement of new partnerships and JVs, the shift to on-chain finance will continue to gather pace in 2026 with key applications for speeding up cross border payments and enhancing global market access in emerging markets.

2026 is set to see AI face its “moment of truth” as a broader proliferation of applications brings the technology firmly into the spotlight. Will AI meet high expectations and enable Banks to continue reducing their cost base and achieving productivity gains amid pressure on revenues? How readily are banks embracing the technology across every facet of the client life cycle and are customer’s ready to integrate new solutions quickly?

Uncertainty linked to the impact of tariffs will continue to see supply chains adapt and change throughout North America and LATAM. Exporters are prevented from circumventing record high tariff barriers through “transshipment” as President Trump set a 40 percent tariff on US-bound transshipments through Vietnam, seeking to undermine Chinese manufacturers rerouting shipments to avoid higher duties. The US President also threatened a ten percent charge on imports from BRICS countries, leading to Brazil shifting its trade policy closer to China.

Demographic changes are also a key area of focus and not confined to wealth management only as a record 31 percent of wealth is concentrated in the “Baby Boomer” generation among individuals aged over 70 in the United States, up from 19 percent in 1990.

Strategic Imperatives

East & Partners Letter to the Market outlines four strategic priorities for Banks in 2026:

- Deepening Relevance: expanding coverage in high growth and fast evolving areas.

- Enhancing Access: faster delivery of insights to decision makers.

- Elevating Impact: embedding insights into execution and avoid overwhelming ‘data dumps’.

- Heightening Customisation: more flexible, dynamic client engagements.

“Volatility will remain the constant. Headlines will keep competing for your attention. And well-meaning voices will continue to predict with confidence what they cannot possibly know. Noise is abundant; clarity is rare. East & Partners will always be on the side of clarity, and we will always champion the true voice of your customer and deliver our clients real evidence-based insights. We are not in the business of guessing the future. We’re in the business of preparing you for it” stated East & Partners Principal Analyst, Paul Dowling.