What’s driving advocacy in business banking? More importantly - where is the ROI?

(6 April 2020 - Australia) Traditional measures of customer advocacy are fundamentally flawed when applied to complex business banking relationships. Of greater concern is the lack of quantifiable return on investment (ROI) outcomes derived from achieving best of breed advocacy performance. Does a high level of preparedness to advocate convert into definable relationship share and revenue growth?

Achieving strong customer advocacy is undoubtedly beneficial in customer retention, however specifically what impact does positive customer recommendations have in real acquisition terms?

What areas of the bank are primary and secondary customers promoting to friends and colleagues? Are they advocating positively or negatively? Should greater focus be placed on containing negative detractors? How long does relationship share take to react to improving ‘mind share’?

Do positive advocators conduct more business with their primary provider? Do positively advocating customers recommend the ‘right’ new clients? And importantly, what are the key drivers behind encouraging business customers to advocate their relationship with you ?

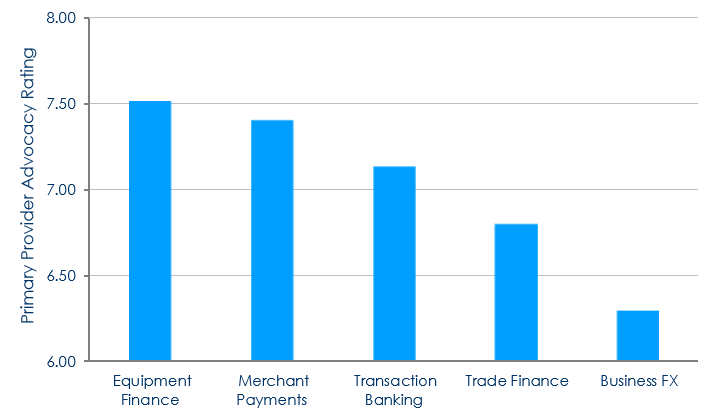

Primary Customer Advocacy – Corporate Segment

Average Rating Reported by Primary Customer

Note: Advocacy rated on a 0 – 10 scale where 0 = negative advocacy and 10 = positive advocacy

Measures of customer sentiment isolating customer satisfaction and advocacy fail to capture the ‘big picture’ customer experience imperative. A combination of customer satisfaction, advocacy and mind share overlaid on relationship share and proprietary market sizing data provides a more accurate understanding of the impact customer sentiment has on bank profitability.

Bank dealings have become increasingly antagonistic as customers grow frustrated by longstanding, positive relationships not supporting their debt funding needs, coupled with rapidly changing regulatory needs and new rules of engagement.

Citing frustrating onboarding difficulties, poor value for money and a lack of understanding of pressing sector and business challenges, CFOs and corporate treasurers are now voting with their feet. Churn intentions have finally reacted to rising levels of dissatisfaction and negative advocacy, lifting from record lows in the wake of tighter credit conditions following the Global Financial Crisis.

At the same time, banks continue with an increasingly strident customer satisfaction based mantra, and indeed have made it their new public battle ground, even though customers appear to have walked away from such claims as having little to do with their real banking experience.

East and Partners demand-side analytics confirm deteriorating customer satisfaction and loyalty across the board. Driven by credit experiences and a strongly perceived lack of provider choice and competition for their business, customers appear to have de-coupled their engagement behaviour from holistic measures of customer satisfaction.

“Are you or are you not satisfied with your business bank” simply isn’t predicting customer engagement and ROI objectives accurately.

The framework leading to this program’s enhancement is quantifying underlying customer sentiment broken down by satisfaction, advocacy and mind share drivers. These insights guide strategic recommendations for improvements in financial performance based on measures of relationship share growth, principally with existing primary customers gauged by wallet share followed by new customer acquisition measured by relationship share.

The supplementary analytics are based on the same representative report sample size, allowing for the data to be segmented by state, enterprise segment and sector.

“The prevailing simplistic approach to what is a complex problem in Australian business banking has resulted in major banks largely failing to achieve real improvement in customer sentiment and loyalty. Across all of our research, we are tracking sharp increases in customer churn intentions as a direct result of this impulse – clients are finally voting with their feet” commented East & Partners Head of Markets Analysis, Martin Smith.

“More importantly how is positive customer advocacy reliably monitored from a value perspective? Are newly recommended customers fully fledged primary customers or do they only transfer one-off or infrequent transactions? That is the key next step that needs to be made beyond whether customers will recommend positively or negatively, because for the most part advocacy remains negative market wide regardless” Mr Smith added.

Contact East & Partners to access Customer Sentiment Monitor analytics or enhance your existing research program subscriptions today - info@eastandpartners.com

Subscribe

Subscribe