Institutional Segment Hunkering Down

(13 October 2014 – Australia) Rapid deleveraging by Australia’s Top 500 companies is continuing, casting doubts over a revival in business lending acting as an alternative growth area for banks facing potential curbs on residential mortgage growth.

East & Partners Deposit Funding & Debt Index (DFDI), created from overlaying the firm’s proprietary demand sized segmentation over APRA’s monthly banking statistics, is a valuable window into the balance between deposits and lending in the banking system.

The latest round of the DFDI reveals institutional business deposit volumes climbing steadily higher, from 18.6 percent of total market deposits in 2012 to a current high of 28.4 percent.

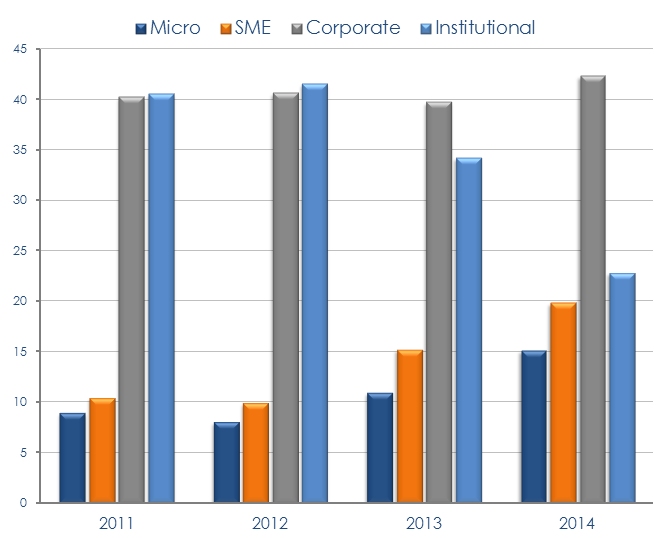

Business lending volumes by the Top 500 have correspondingly contracted, from a 2012 high of 41.5 percent to a fresh low of 22.8 percent in 2014.

This relationship is reflected in the Business DFDI ratio for the institutional segment which increased significantly from 0.45 to 1.25 in the last two years.

This ratio means that Australia’s largest enterprises by revenue now deposit $1.25 for every dollar they borrow. Two years ago, they had 45 cents in deposits for every dollar they borrowed.

Lower wholesale funding costs have allowed for reductions in term deposit rates, benefitting regional banks in particular given they fund the majority of their loans from domestic deposits.

The Top 500 increasingly favours shorter dated Term Deposit tenors, allocating 77.3 percent of volumes to 3 month Term Deposits compared to a mere 0.2 percent to longer dated 12 plus months Term Deposits.

Despite a considerable expansion in SME lending appetite their percentage of total market borrowing volume remains narrowly below 20.0 percent, compared to 42.3 percent for the Corporate segment and 15.1 percent for Micro Businesses.

“The ability to pinpoint which business segment new lending demand will be derived from is critically important to Australian banks in terms of efficiently allocating their resources and valuing the Big Four’s respective propositions among these segments” Senior Markets Analyst Martin Smith states.

“The DFDI accurately tracks trending changes in business deposit and lending volume by segment and bank over an extended time period, providing a forward dated indication of where underlying credit demand is building.

“Australian banks business credit growth rose to almost 5 percent in June 2014 - the highest level in over two years – yet the importance of the SME and Corporate segments in supporting further growth cannot be understated.

“Whether the Top 500 is hoarding cash in anticipation of difficult trading conditions or edging back from an unprecedented period of CAPEX expansion is unclear. For business lending growth to take-off the middle market continues to provide the foundation for new credit demand, in particular the Corporate segment”

Business Lending Volumes by Segment

% of Total Market

Source: East & Partners Deposit Funding & Debt Index

About the East & Partners Deposit Funding & Debt Index

East & Partners monthly Deposit Funding and Debt Index (DFDI) provides insightful research supporting the implementation of bank funding strategies within a constrained and competitive lending market. The industry benchmarks are based on monthly deposit and lending data released by the Australian Prudential Regulation Authority (ARPA). Capturing trending data across core deposit funding and lending metrics allows unique insights to be derived, including business to retail deposit volume ratios, deposit and lending market share, rate triggers for deposit switching, deposit churn levels and tenure of term deposits.

Business Depositor Segments:

› Institutional – A$725 million plus

› Corporate – A$20-725 million

› SME – A$5-20 million

› Micro – A$1-5 million

For more information or for further interview based insights from East & Partners on this report, please contact:

Jennifer Rondolo

Marketing & Communications

East & Partners

t: +61 2 9004 7848

m: +61 411 395 157

e: jennifer.r@eastandpartners.com

Subscribe

Subscribe